BitViraj Technologies - Your Gateway to

Tomorrow's Innovations

Deposit Tokenization: Architecture, Global Pilots, and the Future of Tokenized Banking

Deposit tokenization represents a paradigm shift in the architecture of money and banking. It involves converting commercial bank deposits into digital tokens on distributed ledger technology (DLT), enabling these liabilities to move and settle directly on blockchain networks.

By Bitviraj Technology

April 15, 2024

Deposit Tokenization

Architecture, Global Pilots, and the Future of Tokenized Banking

Deposit Tokenization: Architecture, Global Pilots, and the Future of Tokenized Banking

Executive Summary

Deposit tokenization represents a paradigm shift in the architecture of money and banking. It involves converting commercial bank deposits into digital tokens on distributed ledger technology (DLT), enabling these liabilities to move and settle directly on blockchain networks. This transition from traditional clearing rails to programmable tokenized networks promises instant settlement, enhanced transparency, and seamless interoperability with other tokenized assets.

Major global financial institutions, including JPMorgan, HSBC, Citi, and UBS, have already launched or are actively piloting tokenized deposit infrastructure, with JPMorgan's Kinexys platform processing over $1.5 trillion in transactions. This article provides a comprehensive analysis of this rapidly evolving landscape, covering the core technical architecture, a detailed review of 25 global bank pilots, a case study on India's unique approach integrating with its Central Bank Digital Currency (CBDC), and a comparative analysis with stablecoins and CBDCs. The analysis concludes with strategic implications for banks, investors, and national economies, forecasting that tokenized money will become the default settlement layer for digital capital markets by 2030.

1. Introduction: The Evolution of Money

Traditional banking infrastructure relies on a complex web of core banking ledgers, clearing houses, and settlement networks. These legacy systems, while robust, introduce inherent inefficiencies: settlement delays (T+1 or T+2), significant reconciliation complexity, and high operational costs.

The evolution of digital money has progressed through several distinct stages:

- Electronic Bank Money: The foundational shift from physical cash to digital records on core banking systems.

- Mobile Payments: The decoupling of payments from physical cards and branches (e.g., UPI, card networks).

- Stablecoins & Crypto Payments: The introduction of blockchain-based money for decentralized finance and global transfers.

- Central Bank Digital Currencies (CBDCs): The digitization of central bank liabilities for retail and wholesale use.

- Tokenized Deposits: The digitization of commercial bank money on blockchain networks.

Tokenized deposits represent the confluence of these trends, combining the institutional trust and regulatory safeguards of commercial banks with the programmability, efficiency, and innovation potential of blockchain technology. They are not a new form of money, but a new, more efficient representation of existing bank money.

2. Understanding Deposit Tokenization

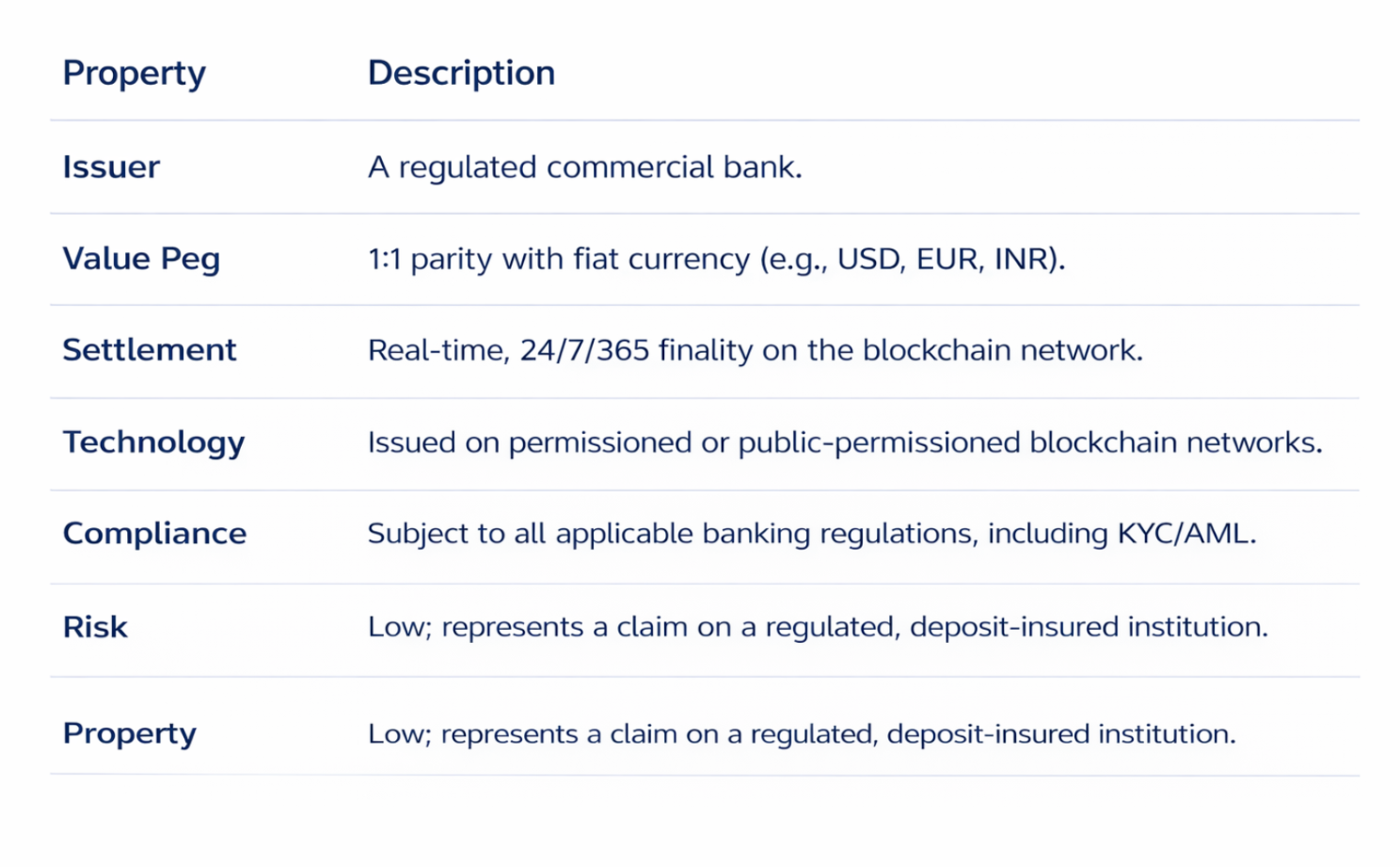

2.1. What is a Tokenized Deposit?

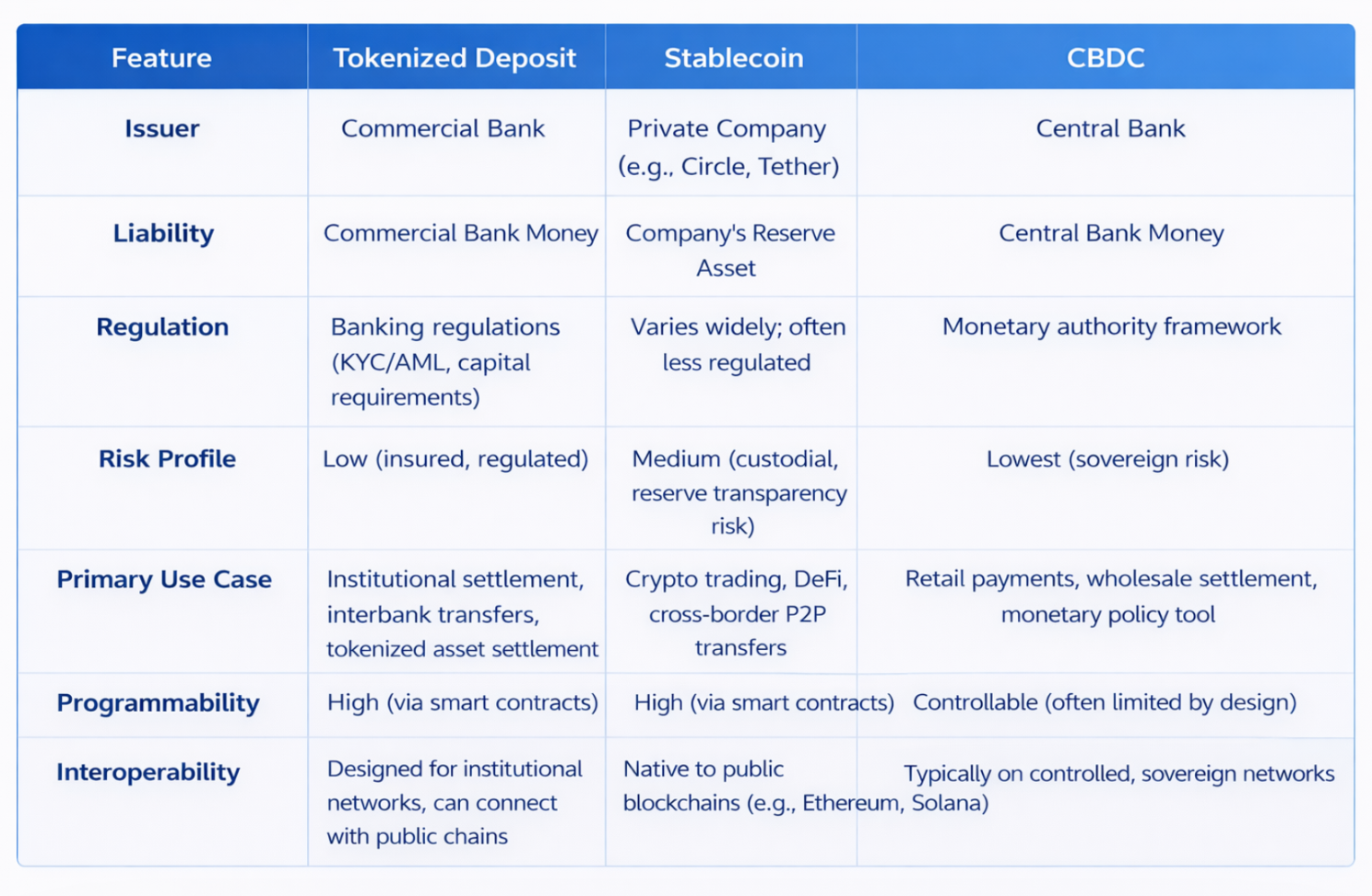

A tokenized deposit is a digital representation of a conventional commercial bank deposit, issued as a token on a blockchain network. It remains a direct liability of the issuing bank and is redeemable 1:1 for fiat currency.

Example: A corporate client deposits $1 million with its bank. The bank's tokenization platform then mints 1 million deposit tokens on a permissioned blockchain and transfers them to the client's digital wallet. These tokens can then be transferred to another client of the same bank (on-ledger) or, through an interbank mechanism, to a client at a different bank, all without moving funds through traditional clearing systems.

2.2. Key Characteristics and Value Proposition

3. Market Size and Industry Momentum

$5–16T

Tokenized asset market forecast by 2030

$650–700B

Monthly stablecoin transaction volume

$1.5T+

JPMorgan Kinexys processed volume

4. The Strategic Imperative: Why Banks Are Tokenizing

Instant Settlement

Real-time, 24/7 final settlement, eliminating counterparty risk and reducing locked capital.

Programmable Finance

Smart contracts automate escrow, conditional payments, and interest distribution.

Tokenized Capital Markets

Natural settlement asset for tokenized bonds, funds, and real estate.

Enhanced Treasury Management

Real-time visibility and control over corporate liquidity.

New Revenue Streams

Banking-as-a-service and value-added services on programmable money.

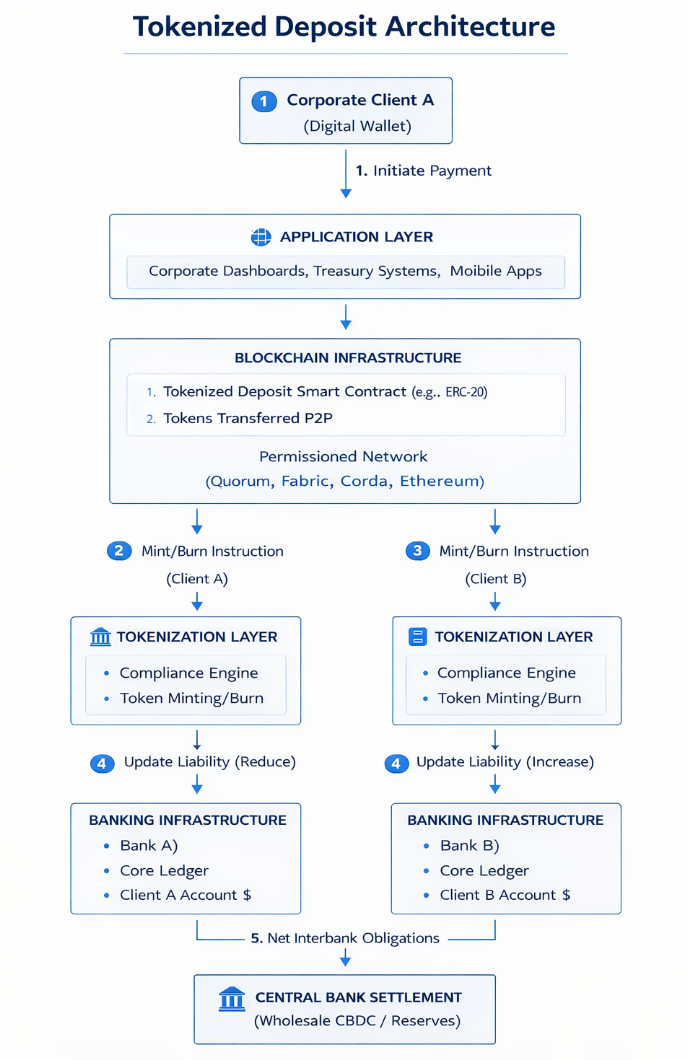

5. Technical Architecture of Tokenized Deposits

A robust and secure tokenized deposit system requires a multi-layered architecture that bridges legacy banking infrastructure with blockchain networks.

5.1. Core Architecture Layers

Layer 1: Banking Infrastructure (Core Systems)

Components: Core banking ledger, customer account databases, KYC/AML systems, compliance and risk management platforms.

Function: This is the system of record for the underlying fiat deposit. The token is always a representation of a balance held in this layer.

Layer 2: Tokenization Layer (Middleware)

Components: Token minting/burning engine, compliance and identity module, API gateways.

Function: This layer acts as the bridge. It receives instructions from the core banking system to mint (create) or burn (destroy) tokens. It also enforces compliance rules (e.g., whitelisting wallets) on the blockchain network.

Token Standards: Common standards include ERC-20 (Ethereum), ERC-3643 (for permissioned tokens), and various proprietary standards on enterprise platforms.

Layer 3: Blockchain Infrastructure (DLT Network)

Components: The distributed ledger, consensus mechanism, nodes operated by banks and potentially regulators.

Function: Provides the shared, immutable ledger for recording token transfers and balances. It is the settlement layer for the tokens themselves.

Common Networks:

- Quorum (JPMorgan): An enterprise-focused variant of Ethereum.

- Hyperledger Fabric: A modular permissioned framework popular among consortiums.

- Corda: Designed for financial services with a focus on privacy and legal agreements.

- Ethereum (Permissioned/Public): Increasingly used for its robust smart contract capabilities and interoperability with DeFi.

Layer 4: Settlement Layer (Final Money)

Assets: This layer represents the ultimate settlement asset for interbank obligations. This could be a wholesale CBDC (central bank money) or commercial bank reserves held at the central bank. The movement of tokenized deposits between banks triggers a corresponding settlement in this final layer.

Layer 5: Application Layer (End-User Interfaces)

Components: Corporate treasury dashboards, digital wallets, trading platforms, API connections for third-party apps.

Function: The user-facing layer where clients initiate payments, manage balances, and interact with other tokenized assets.

5.2. A Typical Transaction Flow (Interbank Payment)

- Initiation: Corporate Client A initiates a payment to Corporate Client B (at a different bank) from its digital wallet.

- Transfer on Blockchain: Client A's deposit tokens are transferred on the blockchain network to Client B's wallet address.

- Redeem/Issuance at Receiving Bank: The receiving bank (Bank B) verifies the incoming tokens. It then "redeems" the tokens (which are a liability of Bank A) and issues new deposit tokens (its own liability) to Client B's wallet. Alternatively, the original tokens could be burned, and new ones minted.

- Interbank Settlement: At a predefined time (e.g., end-of-day or in real-time), Bank A and Bank B settle the net obligations arising from all such token transfers. This final settlement occurs using central bank money (e.g., wholesale CBDC or reserve transfers).

5.3. Technical Flow Diagram

6. Global Architecture Models

Model 1: Single Bank Token System (Walled Garden)

Example: JPM Coin (in its initial form).

Description: The bank issues tokens on its own private network. Transactions are limited to clients of that single bank. While efficient for intra-bank transfers, it doesn't solve interbank friction.

Model 2: Interbank Token Network (Shared Ledger)

Example: Project Guardian (MAS).

Description: Multiple banks issue their deposit tokens on a shared, permissioned blockchain network. This allows for direct, atomic transfers of value between clients of different banks on the same ledger, dramatically increasing efficiency. This requires significant coordination and agreement on common standards.

Model 3: CBDC Settlement Model (Hybrid)

Example: India's RBI Pilot.

Description: Tokenized deposits and tokenized assets coexist on a programmable platform, with a wholesale CBDC acting as the ultimate settlement asset for interbank obligations. This model combines the benefits of commercial bank innovation with the safety and finality of central bank money.

7. Analysis of Global Bank Pilots

7.1. Tier-1 Bank Initiatives

JPMorgan (Kinexys / JPM Coin)

A pioneer in the space. JPM Coin is a deposit token for institutional clients enabling USD and EUR payments. The Kinexys platform has expanded to include repo transactions and intraday repo, with over $1.5T in processed volume.

HSBC (Tokenized Deposit Service)

Focuses on enabling instant, real-time treasury management and intra-company transfers for its multinational corporate clients, reducing friction in global liquidity management.

Citi (Citi Token Services)

Integrates tokenized deposits with trade finance and payments. It provides programmable liquidity and automates complex workflows like Letters of Credit.

UBS (Tokenized Fund Settlement)

Actively participating in projects like Project Guardian to settle tokenized money market funds using smart contracts, demonstrating the DvP potential of the technology.

DBS (Project Guardian)

Partnered with JPMorgan to create an interoperable network where DBS and JPMorgan clients can trade tokenized assets and move tokenized deposits between the two banks.

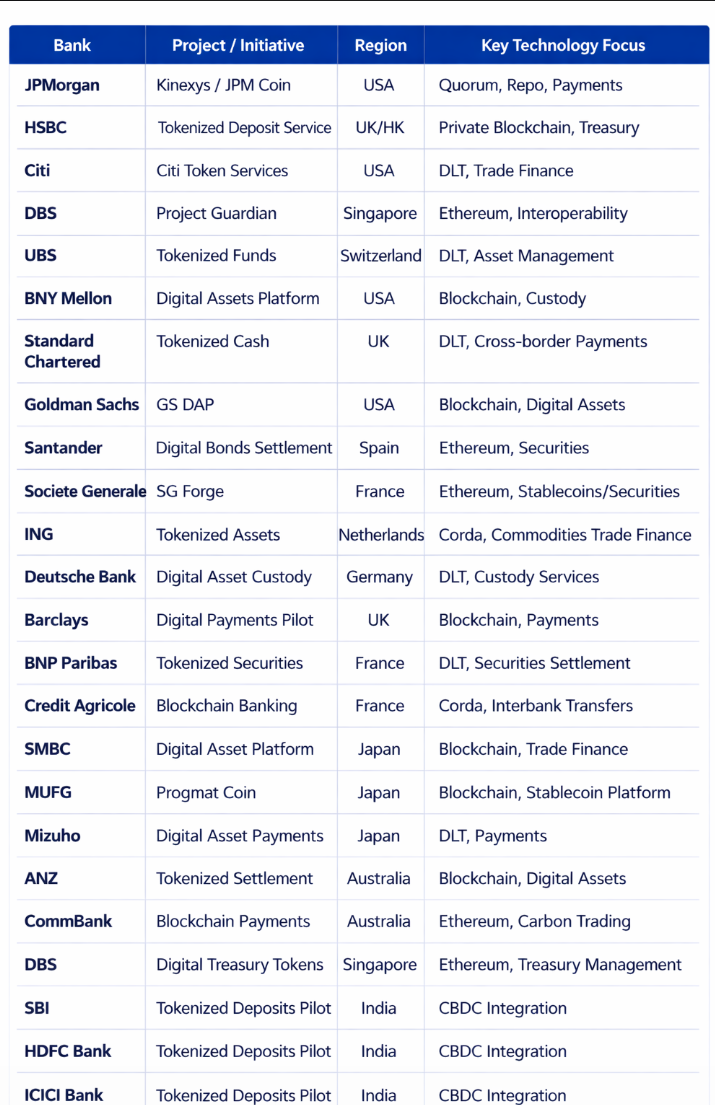

7.2. Comparative Table of 25 Global Bank Pilots

8. Collaborative Industry Frameworks

8.1. Project Guardian (Monetary Authority of Singapore)

A landmark collaborative initiative led by MAS. It brings together policymakers and financial institutions (JPMorgan, DBS, UBS, SBI Digital Assets) to test the feasibility of open, interoperable networks for tokenized assets. Key focuses include:

- Using tokenized deposits for settlement of tokenized bonds.

- Exploring DeFi liquidity pools with institutional-grade controls.

- Establishing industry standards for tokenized assets and deposits.

8.2. BIS Project Agorá

A major project by the Bank for International Settlements (BIS) involving a consortium of central banks and commercial banks. It explores how tokenized commercial bank deposits and a unified wholesale CBDC can be combined on a programmable platform to revolutionize cross-border payments. The project aims to address fundamental inefficiencies in correspondent banking by creating a single ledger where both central bank and commercial bank money coexist.

9. Case Study: India's Emerging Tokenized Deposit Framework

9.1. The Digital Rupee (e₹) Ecosystem

The Reserve Bank of India (RBI) launched pilots for the Digital Rupee (e₹) in 2022. As of 2025:

- 17 banks are participating in the pilots.

- Millions of users and thousands of merchants are involved.

- Two primary versions exist: e₹-W (Wholesale) for interbank settlements and government securities, and e₹-R (Retail) for person-to-person and person-to-merchant payments.

9.2. Tokenized Deposit Pilots in India

Building on the e₹ infrastructure, the RBI is facilitating pilots for tokenized deposits. Major banks including State Bank of India, HDFC Bank, ICICI Bank, and Axis Bank are participating.

The Indian Model:

- Infrastructure: Tokenized deposits are being tested on a permissioned blockchain platform, closely integrated with the e₹-W.

- Mechanism: When an interbank tokenized deposit transfer occurs, the corresponding net settlement is executed atomically using e₹-W. This creates a powerful hybrid model where commercial bank money (tokenized deposits) moves on a programmable ledger, with the final settlement risk eliminated by the simultaneous transfer of central bank money (CBDC).

- Goal: To dramatically improve settlement speed, enhance transparency in financial markets, and create a foundation for a truly unified digital finance stack.

10. Comparative Analysis: Deposit Tokens vs. Stablecoins vs. CBDC

11. Key Use Cases Across Financial Services

Cross-border Payments

Dramatically reduces cost and settlement time by removing layers of correspondent banks.

Tokenized Securities Settlement

Enables atomic Delivery-versus-Payment (DvP) for bonds, funds, and equities, eliminating settlement risk.

Trade Finance

Automates complex workflows like Letters of Credit, releasing payments instantly upon fulfillment of conditions (e.g., arrival of goods).

Corporate Treasury Management

Provides real-time visibility and control over global liquidity, enabling automated sweeps and intra-company settlements.

Real-World Asset (RWA) Tokenization

Serves as the native settlement currency for trading tokenized versions of assets like real estate, commodities, and art.

Programmable Payments & Escrow

Enables conditional payments for large transactions, M&A, or project financing, with funds released automatically by smart contracts.

12. Risks and Challenges

Regulatory Fragmentation

A lack of harmonized global standards and regulations could create legal uncertainty and hinder cross-border interoperability.

Liquidity Fragmentation

If tokenized deposits are issued on multiple incompatible networks, it could fragment liquidity rather than unify it, reducing efficiency.

Cybersecurity & Smart Contract Risk

The reliance on code introduces new vectors for cyberattacks and bugs. Robust security audits and fail-safe mechanisms are critical.

Technology & Integration Complexity

Seamlessly integrating blockchain networks with decades-old core banking systems is a significant technical challenge.

Legal & Compliance Uncertainty

Questions around the legal finality of on-chain transfers, insolvency treatment of tokens, and cross-jurisdictional compliance need to be addressed.

13. Future Outlook and Strategic Implications

13.1. The Vision of a Unified Financial Ledger

The future of finance points toward unified, programmable platforms where different forms of money and assets coexist and interact. In this vision:

- Tokenized deposits (commercial bank money) handle the vast majority of daily transactions and client-facing activity.

- Wholesale CBDC (central bank money) serves as the ultimate settlement asset, providing safety and finality for interbank obligations.

- Tokenized securities (bonds, equities, funds) are issued, traded, and settled on the same ledger using tokenized money.

13.2. Strategic Implications for Global Banks

- Transform or be Transformed: Tokenization is not an incremental upgrade but a fundamental redesign of financial infrastructure. Banks that fail to adapt risk being disintermediated by more agile competitors and new fintech models.

- Focus on the Platform: The future competitive advantage will lie not just in owning deposits, but in offering a platform for programmable finance, data insights, and value-added services built on top of tokenized money.

- Collaboration is Key: Success requires collaboration with other banks, technology providers, and crucially, regulators to establish common standards and interoperable networks.

13.3. Strategic Implications for India

India is uniquely positioned to leapfrog legacy infrastructure. A strategic integration of its three digital public goods—UPI (for retail payments), e₹ CBDC (for settlement), and tokenized deposits (for commercial bank money)—could create the world's most advanced and unified digital finance stack. This would:

- Enhance financial inclusion.

- Increase efficiency in capital markets.

- Position India as a global leader in financial technology and innovation.

14. Investment Opportunities

Tokenization Infrastructure Providers

Companies building the core software and platforms for issuing and managing tokenized deposits.

Compliance & Identity Platforms

Solutions that integrate KYC/AML and other regulatory requirements into blockchain workflows.

Blockchain Security & Auditing Firms

As smart contract risk grows, so will the demand for specialized security audits and monitoring services.

Interoperability & Settlement Networks

Platforms and protocols that connect different tokenized deposit networks with each other and with legacy systems.

Asset Tokenization Platforms

Platforms that tokenize real-world assets will create the demand for the tokenized money to settle them.

15. Conclusion: The Future of Money is Programmable

Deposit tokenization is far more than a technological upgrade; it is a fundamental redesign of how money moves and how financial markets operate. By migrating from fragmented, batch-processed legacy rails to unified, real-time, and programmable blockchain networks, tokenized deposits unlock a new era of efficiency, transparency, and innovation.

As the analysis of 25 global pilots demonstrates, this is not a theoretical exercise but a live, rapidly accelerating transformation. From JPMorgan's multi-trillion dollar repo platform to India's integration with its digital rupee, the infrastructure for the future of money is being built today. The strategic imperative for banks, investors, and nations is clear: embrace this shift, or risk being left behind in the next evolution of the global financial system. The future of money is not just digital; it is programmable.

Case Studies

Empowering Digital

Evolution

Blogs

Empowering Digital

Evolution

BitViraj Technologies - Your Gateway to

Tomorrow's Innovations

Embark on a DigitalJourney

The next-generation digital technology company Bitviraj has the potential to empower and reinvent business in the current fast-paced market.

Our Service

- Website Development

- Application Development

- Blockchain Development

- Gaming and Metaverse